How the sale-lease-back treadmill ends

Subscribe to our newsletter and receive weekly analysis like this for free

This analysis was sent out as part of our weekly newsletter. You can receive it for free by subscribing below:

What GOL’s bankruptcy tells us about the limits of the SLB treadmill

Airline: “Here’s the deal: You buy my airplane, and I’ll lease it back from you. But I want you to pay more than I paid for it, and I’ll increase how much money I give you each month.”

Lessor: “So, I give you extra cash and you pay me back with that cash?”

Airline: “Yeah, deal?”

Lessor: “Deal.”

The sale-lease-back transaction (SLB) has existed in commercial aviation for years. It’s nothing new.

Selling the aircraft for more than you paid for it and leasing it back at a higher rate is nothing novel either. Some call it the “overtrade,” and it has been a successful way of raising cash for growing airlines.

Much has been made of Frontier’s booking gains from SLB overtrades during the first quarter of 2024. This is nothing new for Frontier, nothing new for U.S. airlines, and certainly nothing new for the global industry.

What is new is how the gains from these overtrades are reported. Frontier recently considered them revenues (negative operating expenses, to be precise). Doesn’t change anything for the finances of the airline, just how the numbers are reported. Fair enough.

But while the North American world remains fascinated with where Frontier puts its numbers, the rest of the world says, “Hold my beer, watch this.”

More accurately, “Hold my cerveja…”

The SLB overtrade works like this: You sell the airplane for more than you bought it. That generates cash, but it also generates higher lease payments. Hopefully, the aircraft generates profit, and that profit pays the higher lease rates while the cash is used to grow the business.

But sometimes, it doesn’t work that way. Sometimes, you need the cash from one SLB transaction to pay the higher lease rates from the others.

This is what we call the “SLB treadmill,” and GOL is what happens when the treadmill ends.

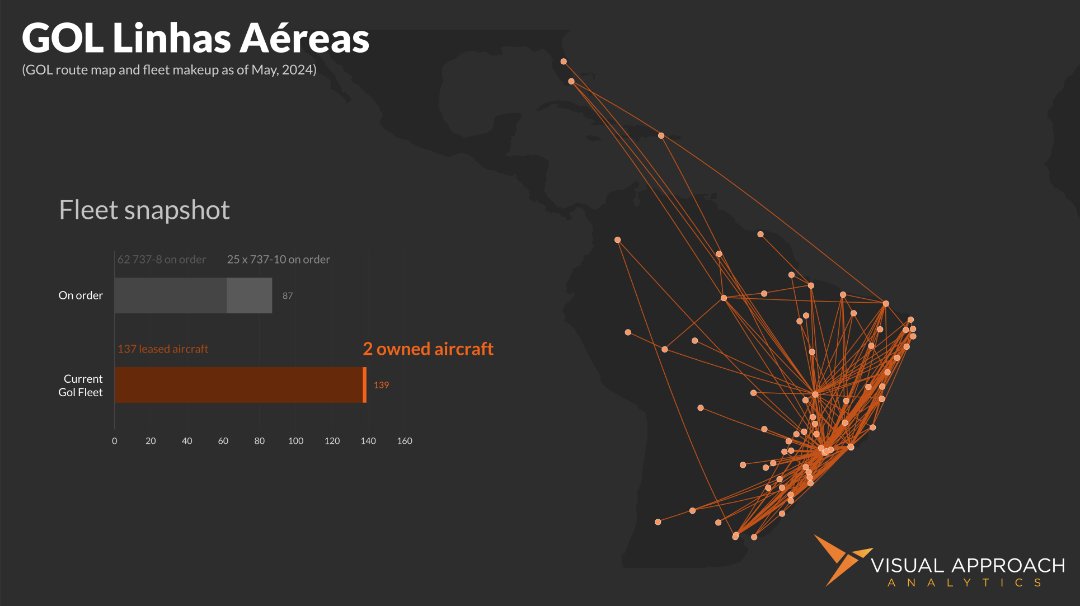

GOL currently controls 139 aircraft. Of those 139 aircraft, GOL owns two. 137 are owned by lessors and leased to GOL. Not all of these aircraft were necessarily sale-lease-back, but many were.

At the same time, GOL has 87 aircraft on order – as in GOL will buy the aircraft then sell them directly to a lessor for some extra spending cash with a higher monthly payment.

However, each aircraft that delivers under an SLB increases the new monthly payments for the fleet. The first aircraft may net you $10 million for an additional $100,000 per month, giving you just over eight years to use the cash to pay back the extra.

But the 100th aircraft will net you $10 million while your cumulative lease rate increases now amount to $10 million per month – one airplane a month must be delivered just to pay for the extra cash you took (and probably spent).

The delivery treadmill has to keep running to fund the airline. What happens when the deliveries can’t keep up?

If you’re not generating a profit from the operation long enough, the treadmill ends. For GOL, it was a Chapter 11 bankruptcy filing.

Paradoxically, Boeing’s inability to deliver 737s to GOL at a rate that funded the rest of the operation likely prematurely ended the treadmill. Were those aircraft needed? That’s a different question.

It’s this treadmill that triggered concerns following Frontier’s earnings call. Only, if Frontier is on the treadmill, it’s not moving at a very fast pace, yet.

The point is to be able to invest the extra cash from the overtrade to slow down the treadmill before it shoots you off the end. That comes by way of a profitable operation.

Frontier does not currently have a profitable operation. But it does have a long way to go before anything becomes problematic. Just like many other airlines that have benefited from sale-lease-back transactions.

The treadmill, itself, isn’t necessarily bad. But, like my father loves to remind me:

“It’s not the fall that kills you. It’s the sudden stop at the end.”

Dad

faça um teste:

GOL is still a powerhouse in Brazil. The question is, where?

We’ll spot you its largest market. São Paulo Congonhas Airport (CGH).

What markets round out the remaining ten?

The answer:

Now for the next test. Can you name each code?

Subscribe to our newsletter and receive weekly analysis like this for free

This analysis was sent out as part of our weekly newsletter. You can receive it for free by subscribing below: