Painful end to a 53-year streak

Subscribe to our newsletter and receive weekly analysis like this for free

This analysis was sent out as part of our weekly newsletter. You can receive it for free by subscribing below:

The hard truth behind Southwest’s historic layoffs

This analysis did not go the way I thought it would.

It happens. I’ll dive into some numbers to show what I think is happening, only to find that the data points in a different direction than expected. This is one of those times.

On Monday, February 17, Southwest Airlines announced its first layoffs in 53 years. 1,750 administrative staff were delivered separation notices, representing approximately 15 percent of the total back-office employees.

This is a big deal—a VERY big deal. Southwest has long been the icon of great places to work. Breaking the enviable 53-year streak while the company is profitable is a sign that the company has changed. There is no other way to look at it. Southwest just jumped the shark.

Of course, the takeover by Elliott Management earlier this year certainly has much to do with the decision to end the 53-year streak. And yes, despite whatever deal was struck, we consider it a hostile takeover. The about-face on layoffs this Monday leaves no doubt.

But there is more to the story.

First, why did Elliott push Southwest to risk everything that made Southwest what it is today?

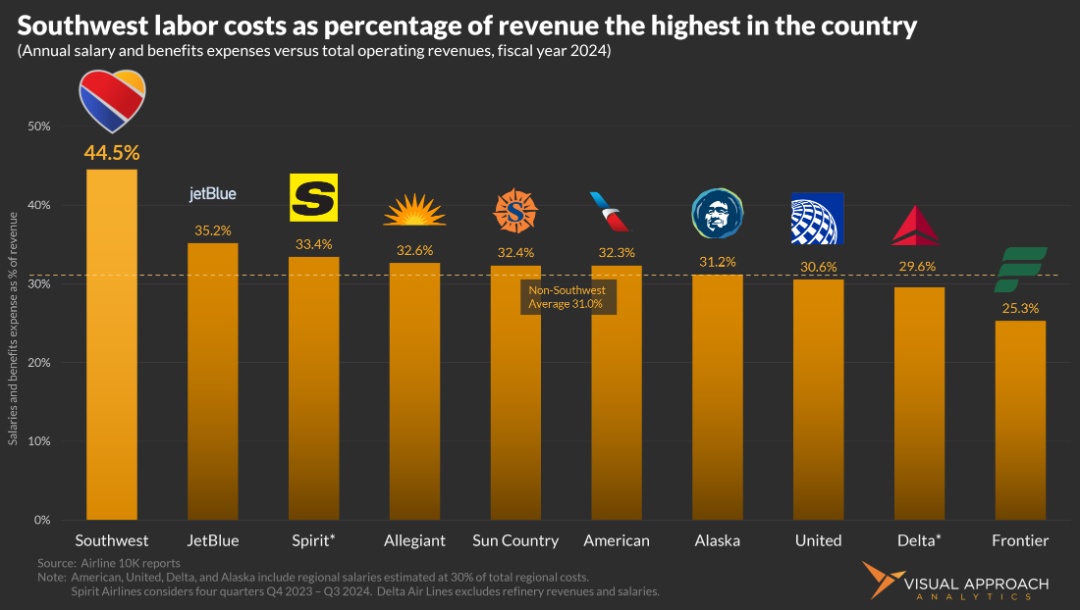

Southwest hired too many people. There is no ignoring that the airline’s labor costs are out of line with the rest of the industry.

In 2024, almost 45% of Southwest’s revenues went to pay employees. For context, the industry average without Southwest is 31%. The next-highest airline is JetBlue, which pays 35% of its revenues in salaries and benefits. The next seven airlines are all clustered between JetBlue’s 35% and Delta’s 30%. That shows just how out of line Southwest is.

Frontier currently has the lowest amount of revenues paid in salaries and benefits at 25%. However, the airline has yet to negotiate a pilot contract all other airlines have completed with massive raises. The Frontier number will go up.

But not to 45%.

And that’s the problem. Southwest’s labor costs are out of whack. No matter which way we look at it, Southwest has a problem. At the same time, Elliott is not in the business of maintaining 53-year streaks or even operating anywhere near the “best places to work” lists.

But this gets back to the fundamental question. How valuable is company culture?

To be certain, this is not a question to be answered by Elliott; however, it was priced by the activist investor. That price was $510 million — the labor costs expected to be saved by the cuts over the next two years.

But Southwest did have too many people. The numbers are very clear.

Yet, the questions surrounding Elliott’s hostile takeover of Southwest never centered on whether Elliott could make money. The questions centered on what would be left of Southwest after Elliott.

As of market close on Wednesday, Wall Street was not sure. Southwest’s stock ended the day down after the first day of trading on Tuesday, only to recover to Friday’s close by Wednesday. No sign of a $510 million windfall over the next two years from Wall Street; rather, it was an implied acknowledgment that there was some tradeoff. A stagnant stock price and simple back-of-the-napkin math suggest Wall Street values the impact on company culture and future lost revenues from the layoffs, around $510 million over the next two years. (hey, don’t knock the napkin. Plans sketched on a napkin led to the 53-year streak to begin with.)

As for us, we don’t know just how forgiving Southwest’s customers and employees will be on the about-face. Can the company continue to bring in the same revenues without the 1,750 employees? Why did they hire so many in the first place? We don’t know what the future of Southwest holds after heading down the Elliott path, but it’s happening.

We do know that Southwest had too many people on the payroll. But we don’t know that the 15% band-aid being ripped off was the right answer. The market doesn’t know either.

We just thought free bags would go first.

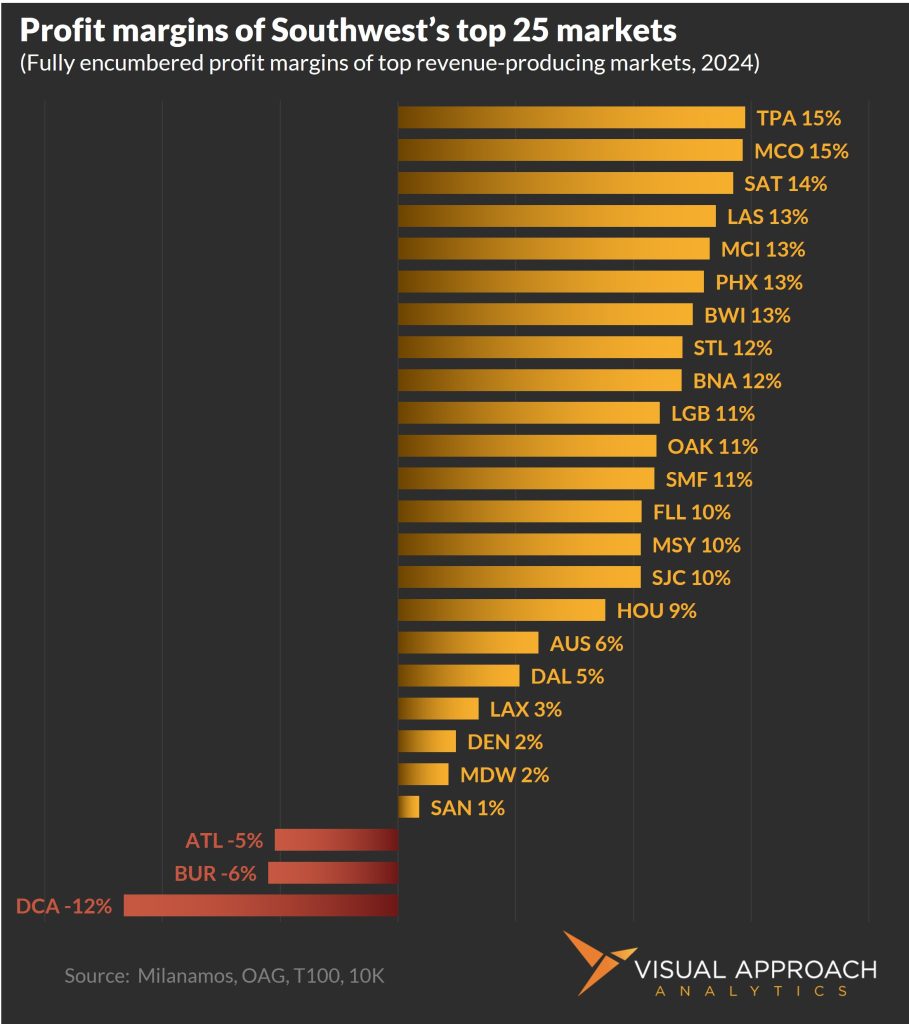

Pop quiz – Profitability in Southwest top markets

We’ve been working with clients on network profitability models for some time. This week feels like the right time to examine how Southwest’s largest cities performed during the year.

Only, we’re not going to tell you which ones they are.

These are the top 25 airports by pro-rated revenues. Straight-line pro-rate, fully allocated costs for the year.

When you think you’ve got the answers (or you’ve given up), you can find the answer here.

The answer:

Southwest’s network profitability is a tale of differing neighbors. Florida makes money for Southwest – at least by our estimates. Georgia? Not so much.

LAX squeaks a profit while Burbank struggles.

BWI? Good. DCA? Oh, so bad.

These are just the top 25 markets. There are dozens of others.

The worst performing market? ITO (Hilo, HI).

Highest margin? PBI (West Palm Beach, FL).

But also consider that arriving at these numbers requires an aligned philosophy on how to handle costs. We know within a narrow band of uncertainty what it costs to operate an aircraft. We also know how much overhead the airline carries. But how should that overhead be attributed to individual flights? As a percentage of revenue? Per passenger? Per ASM, or block hour, or mile flown?

We chose per passenger. It’s not entirely a per-passenger cost, but we kept it simple. It could be argued that the majority of overhead is built to support the passenger rather than how far that passenger flew or what they paid. Some costs are associated with fleet size, number of airports, etc. but we found this a good approximation.

Subscribe to our newsletter and receive weekly analysis like this for free

This analysis was sent out as part of our weekly newsletter. You can receive it for free by subscribing below: